Home » Divorce and Family law Blog » Dividing a 401(k) in California Divorce: Avoid Expensive Errors

Founder Attorney-Mediator and California's Top-Rated Super Lawyer

Dina Haddad and her team provide expert mediation services for Californians. If you want help related to any family law issue, call us or book a consult.

Sarah thought splitting her husband John’s 401(k) during the divorce would be simple. The community had an interest in $400,000.00 so she would receive 50% or $200,000.00.

They agreed and her attorney prepared the Marital Settlement Agreement stating she would receive the $200,000.00 from the 401(k) plan.

After the divorce was final, Sarah tried to receive her $200,000 share, but the plan administrator rejected it. Why? No QDRO was prepared.

A Marital Settlement Agreement is insufficient to transfer funds from an employee spouse to a non-employee spouse from a 401(K) plan. Now she must return to court, pay more legal fees, and hope her ex-husband cooperates.

In reality, a 401(k) is more tricky than dividing money in the bank. The slightest mistake can lead to penalties, taxes, or lost growth. So what should you do?

This guide explains all you need to know about how 401(k) divisions work in California and how to avoid expensive errors. If you need more personalized help out of court and a cost effective solution regarding assets division or 401k, visit our website or book a free consultation with divorce experts like Dina Haddad in California.

During a divorce, California courts apply a significant amount of review and scrutiny when reviewing a 401(k). But despite it being one’s personal savings, it is treated as community property and divided according to community property rules. Learn more about community property exceptions.

However, not every portion of a 401(k) is divisible during a divorce. If a party contributed to the 401(k) prior to marriage or after the date of separation, that party can prove that portion to claim it as their separate property. If done, that portion is not divided between the parties.

Contributions during the marriage, and the growth on those contributions, until the retirement is divided, are considered community property. The burden to prove separate property contributions rests with the separate property owner.

The court will not do the work to validate a party’s separate claim. Instead, the court will review a separate property owner’s claim to determine if it is sufficient to evidence their separate property. If the separate property is not proven, the retirement shall be equally divided.

To fairly divide a 401(k) account, the process has to adhere to both federal law and California family law. California family law dictates that retirement accounts during marriage are divided 50/50 absent a party demonstrating that a portion of that account is separate property.

The interest includes the market returns on those funds, referred to as earnings and interest. The main federal law controlling how 401(k) plans can be divided and paid out is the Employee Retirement Income Security Act (ERISA).

ERISA generally prohibits transferring retirement plan benefits to anyone other than the participant. This means you cannot transfer retirement benefits to your spouse, without a QDRO. To bypass a QDRO, you can do so only by:

Additionally, any division in family law must comply with the retirement rules. For example, a pension is payable to the employee in monthly payments at retirement age.

The non-employee spouse’s portion will be paid out in a similar manner or according to the plan’s rules for division in divorce. For example, the plan can legally refuse payment if the judge awards a spouse $100,000 payout, but that plan doesn’t allow lump sum payouts.

In other words, the court cannot override the plan’s written rules. Courts cannot order 401(k) plans to pay benefits in ways that are inconsistent with their policies.

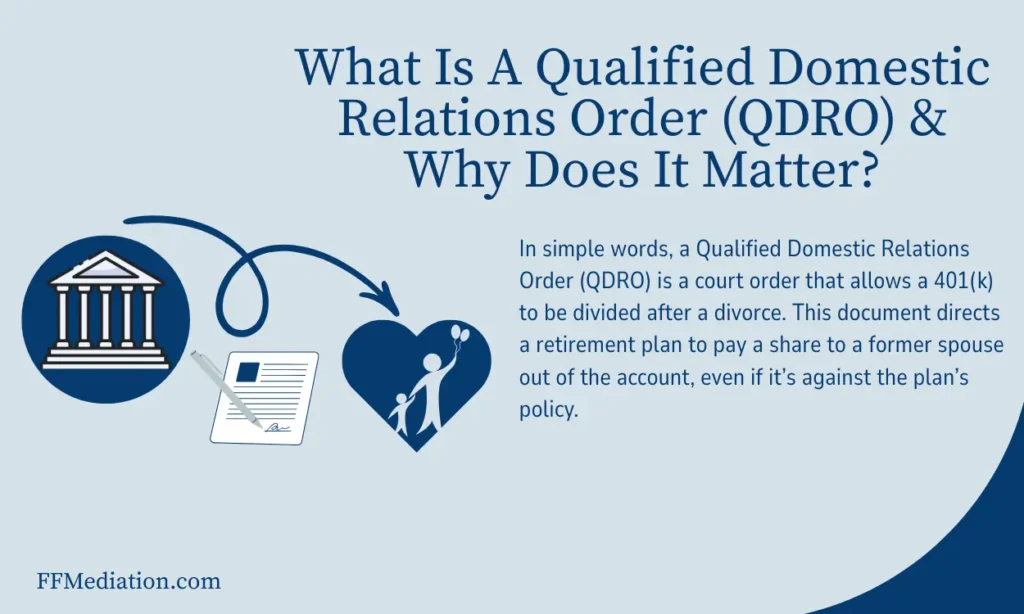

A Qualified Domestic Relations Order (QDRO) is a court order that allows a 401(k) to be divided after a divorce tax-free. This document directs a retirement plan to pay a share to a former spouse out of the account, without penalties and taxes.

Without this court order, the plan is legally allowed to reject a payment request, even if it comes with a signed divorce judgment.

Besides mitigating fraud, a QDRO helps avoid the 10% penalty for withdrawing early. It also makes the funds untaxable if rolled into an IRA immediately after being transferred to the non-employee spouse. Typically, the funds are rolled over directly into a rollover IRA in that spouse’s name.

Both the court and the plan administrator must approve a QDRO. In a case where there are multiple retirement accounts, each one will require its own QDRO for withdrawals.

If the document contains errors in wording or calculation, it can lead to thousands of dollars lost due to penalties or tax consequences.

In California, once the divorce process has begun, there is an automatic restraining order that prevents both spouses from transferring funds from accounts without either each other’s consent or court approval. So, if your spouse decides to cash out their 401(k) early, here’s what happens:

The court will treat the withdrawal as misconduct, and penalties may apply. Additionally, they will also be required to pay the other party their share of the 401(k) funds.

As for taxes and penalties, those will be incurred and handled by the spouse who made the withdrawal and won’t be deducted from your portion.

Suppose the spouse has spent the withdrawn funds, the judge will often add the value of your share of the retirement funds into the marital estate for calculation purposes. In other words, you will be compensated with a larger share of the remaining assets.

Depending on the severity of the case, courts can impose sanctions for poor financial disclosure. Some penalties include giving 100% of the undisclosed asset, facing contempt of court, or monetary sanctions.

There is no legal rule for the number of years required before you can claim a share of your spouse’s 401(k) in California. What matters is how much was contributed to the account during the period of the marriage.

So, even a short marriage can qualify for some community property in the retirement account. The only effect time has on the division of a 401(k) is the amount, as less money is accumulated in 2 years compared to 10.

In rare situations, yes. Your ex can come to claim their share of your retirement funds if these funds were (1) awarded to them in the divorce judgment; or, (2) it was a missed asset and the statutory requirements are met.

If the 401(k) was divided but the QDRO was not completed, the 401(k) is still divisible. The court still has power to issue orders to finalize asset divisions that are part of a divorce judgment. However, you cannot include new orders to divide properly that were already awarded to a spouse.

Your ex can raise a claim if the judge awarded her a 401(k), but no QDRO was approved to withdraw the funds. It may also happen if the judgment reserved jurisdiction over retirement or if drafting errors prevented proper division.

Your ex cannot file a claim if the final divorce judgment clearly divided the retirement account and the QDRO was filed, accepted, and implemented. Also, depending on the state and the legal specifics of the case, the statutes of limitation may apply, making it invalid to make a claim over your retirement funds.

This depends on how your money was transferred. If you move the funds correctly with a QDRO, you can avoid taxes and penalties. However, if the money was withdrawn as cash, you may have to pay income tax.

This is mainly because cash distributions are often considered ordinary income, meaning that if the transfer is not structured correctly, federal and California state taxes both apply.

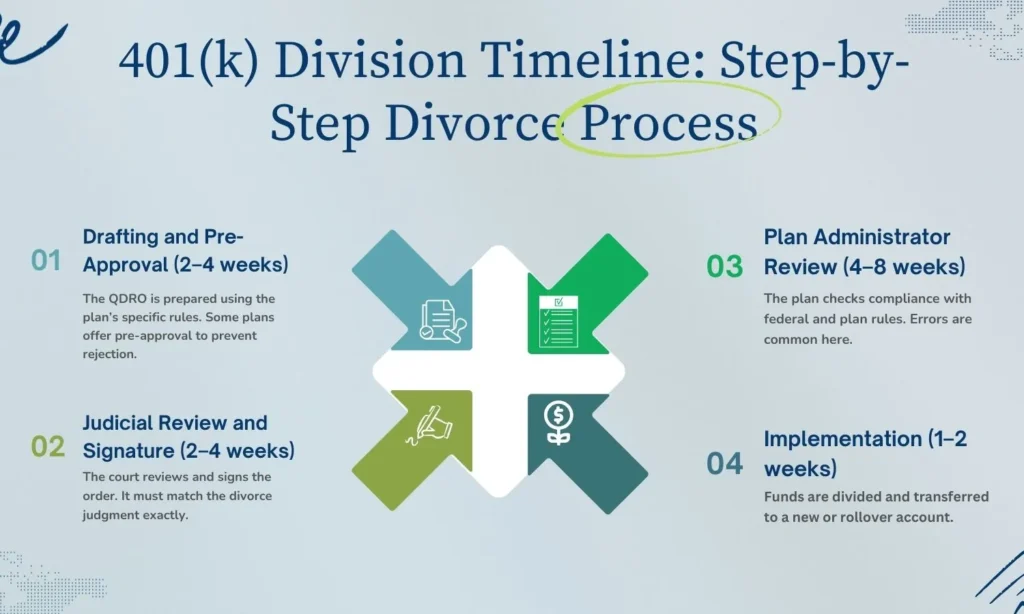

There’s no concrete timeline for when you can take your cash out of the 401(k) account. The process takes time because after the judge gives his judgment, you still need to draft a QDRO, have it approved by the court, and then also have it accepted by the plan administrator.

During this time, expect delays as the employee plan review process can be slow. The account can even lose or gain value, depending on the market, but this can be captured in a properly drafted QDRO.

After the mandatory 6-months waiting period, finalizing your divorce can take time, depending on your specific case and the process you choose. Mediation is often faster than other divorce processes.

Afterward, drafting a QDRO can take a few weeks to months, and getting the plan administrator to review and approve the request can take 1-3 months. There will then be additional time to file the QDRO with the family court. Learn when one should file for divorce in California.

Delays often happen due to filing errors, incorrect QDRO language, failure to follow plan rules, or lack of follow-up from the plan administrator.

The biggest cause for delays are drafting errors, which can require you to restart the whole process. There are also few professionals that offer QDRO services, increasing the timeframe.

The next step after a QDRO is drafted and approved is to pick your mode of withdrawal. This is important because some methods protect your savings, minimize taxes, and leave you with more money than other methods.

One option is rolling the funds into a personal IRA to make it tax-deferred.

Withdrawing cash is the least recommended option because income taxes can apply.

In order to divide a 401(k), parties must proactively complete the rollover process. The court, attorneys and mediators cannot complete the transfer on behalf of the parties.

To avoid common mistakes, pay special attention to:

The smallest oversight can cost you thousands. Avoid them at all costs.

Determining the community and separate value of your 401(k) is important. In order to determine the community portion, you will need the date of your marriage, the date of separation, and the account balance during this period.

This marital portion is then calculated based on documented contributions and growth. While there are online 401(k) calculators, California courts do not rely on them but instead on retirement statements and verified data, such as actuarial or forensic calculations.

This calculation can also be done in reverse by determining the separate property portion, and backing that out of the total retirement balance.

Ending your marriage past 50 has special considerations given parties are closer to retirement age. Dividing retirement accounts can feel especially painful knowing you may have half of your retirement savings so late in your career.

Consider options that will keep your funds invested as much as possible to eliminate lost time in the market. Also consider catch-up contributions as they can help rebuild savings during this time.

Even after the divorce is finalized, the retirement division requires separate steps. Delays often occur during drafting or plan review.

Missing follow-ups with the plan administrator can add months to the timeline. Ultimately, careful coordination reduces rejection and repeated corrections.

The QDRO process often spans 60 to 120 days, though timing varies by plan.

Retirement accounts follow specific legal rules that differ from other assets, like checking accounts or real estate. Retirement accounts are subject to federal laws in addition to state law. Division requires compliance with both.

Remember Sarah? Her 401(k) division was rejected. She lost six months of earning potential and paid thousands in added legal fees because the paperwork was not done correctly.

A 401(k) is not a bank account, but it is often one of the largest assets in a marriage, sometimes worth hundreds of thousands of dollars, built over decades.

Mistakes can trigger income taxes, penalties, and lost growth that cannot be recovered. A properly drafted and approved QDRO, structured rollover, and clear 50/50 division under California law protect your future.

Early guidance from California divorce mediator Dina Haddad can help you avoid costly errors. Schedule a free consult today.

It’s usually best to wait until absolutely needed. While it is possible to avoid the 10 percent early withdrawal penalty for retirement accounts using a court order, income tax will still need to be paid. Also, withdrawing retirement money will lower the long-term value of that money.

A judge could reopen discovery if your spouse did not disclose their retirement account. Your spouse who conceals a retirement account could face fines/monetary sanctions, an unfair distribution of marital property and/or other penalties.

In California all divorcing spouses are required to provide full financial information about their assets during the divorce process.

The division process is similar, but the tax treatment is different. Roth 401(k) contributions are made with after-tax dollars, and qualified withdrawals are generally tax-free.

A proper court order is still required to divide the account. Careful planning helps protect future tax advantages.

Yes. In California, automatic temporary restraining orders usually prevent either spouse from transferring or withdrawing retirement funds without consent or court approval.

If you are concerned about early withdrawals, discuss protective steps during your free consultation with Dina Haddad.